Sum180 as seen in csmonitor.com, By Lisa Rabasca Roepe Contributor

As consumers struggle with credit card balances and meager savings, AI-powered apps offer new ways to take control of their finances. But some say this fresh handle on fiscal responsibility still needs a human touch.

Olivia Moore of Chicago was $20,000 in debt when she downloaded Tally, a personal finance app designed to help customers pay off their credit cards. With Tally’s help, in less than two years, she was able to cut her debt in half. Similarly, Callie Person of Florida turned to an app called Charlie, and in less than a year, she was able to set aside $1,500 in savings.

In a nation challenged not just by debt and tight incomes but also by shortfalls in financial literacy, those are significant victories.

And these apps have a distinctive feature: Tally and Charlie are early examples of deploying artificial intelligence, or AI, to assist with personal finance.

It’s a way for time-strapped consumers to get some nudges – based in part on data about their own past behavior – to align their small daily decisions with longer-term goals. But as with so many technologies, these uses of AI also come with caveats. This early phase of AI-empowered apps may be revealing cautionary lessons that coexist with their emerging promise.

“Technology can do a lot of good things to help people with their finances – especially to assess, to measure and track, to offer curated learning resources, and to nudge and remind,” says Cynthia Meyer, resident financial planner at Financial Finesse, a financial education program. ”But it can’t be empathetic, be a compassionate witness to someone’s struggles or worries, brainstorm in the moment, or offer a nuanced perspective or find the ‘question behind the question’ like a human financial planner can.”

For many people, including 20-somethings like Ms. Moore and Ms. Person, it appears that the caveats don’t outweigh the convenience.

“It doesn’t feel weird or out of the ordinary” to be letting an app like Tally access personal data, says Ms. Moore in Chicago. “I’m a young millennial and have grown up with all forms of technology, including AI. … I understand that to receive a certain level of service, you have to give a certain amount of information, and I’m OK with that.”

And for her, the benefits were visible. Tally issues users a line of credit, enabling the app to make credit card payments for them and then charge a lower interest rate. It also served as a caution flag on debt in a way that credit card statements hadn’t done for Ms. Moore in the past. “Tally reminded me that those rates are very real and are very, very high.”

A big need for financial help

Although millions of consumers now use AI-based finance apps, the apps still lag behind more traditional online financial tools. But proponents see reasons for growth.

These apps are empowering because they show consumers in user-friendly ways how to save money or pay off debt, says Carla Dearing, CEO of online financial wellness service SUM180.

“It’s important to recognize that customers who use banking apps leveraging AI typically have a much higher level of engagement than standalone apps,” says Jody Bhagat, president of Americas at the company Personetics, a provider of AI tools.

And they’re dawning at a time of need.

Most Americans struggle to manage their finances. According to a 2018 Bankrate survey, 20% of Americans aren’t saving any money. Four in 10 Americans couldn’t handle an unexpected expense of $400, according to a 2018 Federal Reserve study.

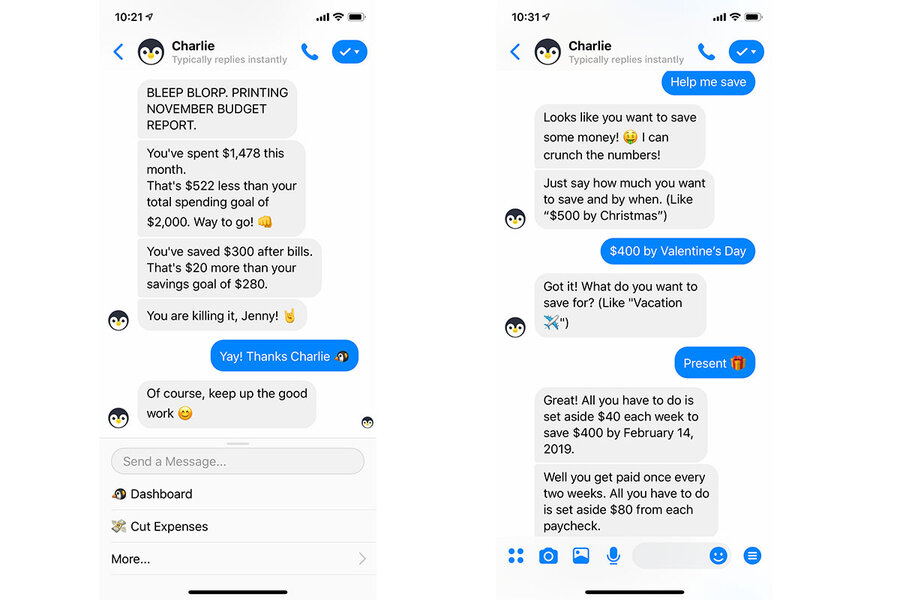

Courtesy of CharlieScreenshots of Charlie in action. The app analyzes daily transactions, so if a user spends more than usual on groceries or take-out, the app flags it. The idea is to give people actionable advice in the moment.

“The big picture is Americans don’t like to manage their finances,” says Thomas Smyth, CEO of Trim, an app that analyzes the consumer’s banking and credit accounts to find subscriptions and recurring payments and then gives the option of canceling them.

“The thing about saving and projecting finances is it’s a hard and an embarrassing conversation to have,” says Brian Wolfe, assistant professor of finance at the University at Buffalo School of Management. It might be easier to interact with a robot than to look a financial planner in the eye and feel like you’re being judged, he says.

The limits of AI tools

Still, many financial experts warn that the AI tools each tend to tackle just one challenge rather than deliver a detailed or individualized long-term financial plan.

Without a financial adviser, says Ms. Dearing at SUM180, it’s difficult to address some of the more complicated issues, such as emotional spending or couples with different spending habits. And if you’re facing eviction or drowning in college loans or credit card debt, an app probably isn’t your answer.

Another challenge: When the AI talks, will consumers listen?

“Sometimes we override apps,” says Bryan Routledge, a finance expert at Carnegie Mellon University’s Tepper School of Business in Pittsburgh. When your Fitbit nudges you to walk, some people just take it off. Similarly, some people will ignore a finance app telling them they’ve already spent their discretionary budget for the month, especially if they’ve just pulled up at Target with a kid who needs a new pair of sneakers.

Is it safe?

The biggest issue might be the amount of financial information you need to disclose to use the apps, says Professor Wolfe in Buffalo. Nearly nine in 10 U.S. banking consumers said they’re concerned about data privacy and data sharing, according to a 2018 report from The Clearing House.

Mary Wisniewski, an analyst with Bankrate, tests out AI-powered savings apps daily, but so far, none are part of her day-to-day life. “I got a little paranoid about the sharing of data,” she admits. Also, the apps don’t fit her money management personality, which she describes as hands-off. She grew tired of receiving “all sort of alerts.”

AI executives are fully aware that consumers are nervous and that a security breach could be a company-ending event. The app companies quoted in this article say they never sell user data, don’t allow advertisers to use data for targeting, and keep the data securely encrypted.

In the end, financial experts say sometimes old technology still has its value, such as the way traditional banking apps can give an automated reminder when your balance is low.

“For consumers the smartest thing they can do is to use direct deposit to save 10 to 15% of your paycheck and have it go automatically into a saving account,” says Mark Schwanhausser, director of digital banking at the advisory firm Javelin Strategy & Research.

But many experts also say that integrating an AI-powered app with a financial coach or planner could be a powerful combination, as long as you understand how to use the technology and have a basic level of financial literacy.

Consumers don’t always understand what the app is telling them to do, says Annamaria Lusardi, founder and academic director of the Global Financial Literacy Excellence Center at George Washington University in Washington, D.C. “You need proper knowledge to make this tool work for you,” she says.

Even Callie Person, who saved $1,500 by using Charlie, warns against relying solely on technology. “Charlie is not a replacement tool for sitting down, creating a budget, and having important conversations about finances with your partner,” she says. She calls it an aide “to help get you on the right track to managing your finances.”